Update: Please note that 2025 updates under the EU Omnibus Regulation may affect certain requirements and timelines. Readers are advised to review the latest Omnibus developments for the most up-to-date context.

To foster responsible corporate behaviour, a number of legislations targeted at supply chain due diligence have been created. Some examples are the German Supply Chain Act, Battery Regulation, Corporate Sustainability Due Diligence Directive (CS3D), and Ecodesign for Sustainable Products Regulation (ESPR).

The Corporate Sustainability Reporting Directive (CSRD) makes it mandatory for large companies and all companies listed on regulated markets to disclose sustainability information. All reported data will need to be digitally tagged and audited, ensuring transparency. While non-compliance could lead to penalties, the rewards for following the rules are significant, such as greater green investment, the chance to turn sustainability efforts into financial value, and a more unified reporting process.

In this article, we will discuss the Corporate Sustainability Reporting Directive in detail, but you can read on to find out more about the key differences between CSRD and CS3D.

What is the aim of the Corporate Sustainability Reporting Directive?

The Corporate Sustainability Reporting Directive creates a common reporting framework that improves the content and quality of sustainability information. Ultimately, the legislation aims to increase the firms’ trustworthiness in the eyes of stakeholders such as investors, banks, customers, and consumers.

In terms of the legislative background, the directive is part of the European Union’s (EU) Sustainable Finance Package, which aims to enhance the flow of money to sustainable activities. The package also includes the EU Taxonomy Delegated Act and six amending Delegated Acts. The directive widens the scope of the Non-Financial Reporting Directive (NFRD) adopted in 2014. Before being fully implemented, the directive has to undergo a complex policy-making process.

What is the timeline for CSRD compliance?

The Corporate Sustainability Reporting Directive (CSRD) was adopted on 21 April 2021 with the aim of standardising and enhancing sustainability reporting across Europe. In July 2023, the European Commission officially adopted the European Sustainability Reporting Standards (ESRS), developed in collaboration with EFRAG. These standards define the specific reporting categories companies must follow. The CSRD has been integrated into the national laws of EU member states since July 2024.

Large firms already subject to the Non-Financial Reporting Directive (NFRD) had to comply with new governance requirements on 1 January 2025. Listed small and medium-sized enterprises (SMEs) must comply from 1 January 2026, while non-listed SMEs can participate voluntarily. Over the coming years, thousands of additional companies will fall under the directive’s scope, with all listed SMEs in the EU required to comply by 2028 at the latest.

The final phase of the policy process will be completed once the detailed reporting requirements are fully rolled out and implemented, ensuring a comprehensive and transparent approach to sustainability reporting across Europe.

Who is subject to the Corporate Sustainability Reporting Directive?

The Corporate Sustainability Reporting Directive expands the reporting requirements to more entities, including those organised as foundations, trusts, or franchises1. In particular, the directive applies to:

- All large companies that meet at least two of the following criteria (applies from fiscal years starting on or after January 1, 2024, for companies already subject to the NFRD, and from fiscal years starting on or after January 1, 2025, for other large companies)some text

- 250 and more employees on average during the financial year 5

- €40M or more in net turnover

- €20M or more in total assets

- Listed SMEs, i.e. those whose financial assets are traded on EU markets (applies from fiscal years starting on or after January 1, 2026)

The directive does not apply to non-listed SMEs and micro-enterprises, but they can opt to comply with the standards voluntarily.

What are the requirements of the Corporate Sustainability Reporting Directive?

Firms will have to disclose detailed information on human rights, the environment, and governance in their management reports. The subject matters will have to be prepared according to the European Sustainability Reporting Standards (ESRS). The ESRS and the double materiality assessment provide detailed frameworks for what to disclose and how to structure the information to broaden traditional reporting and alignment with Europe's broader sustainability goals.

What information should enterprises disclose in CSRD reports?

The EU aims to align its sustainability reporting standards with existing legal frameworks, such as the European Green Deal, Sustainable Finance Disclosure Regulation (SFDR), and Taxonomy Regulation, as well as global sustainability initiatives such as the SDGs and ESG criteria. As a result, the EU sustainability reports will use similar indicators. The standards will also require companies to disclose information that financial market participants must provide under the SFDR. Additionally, businesses will need to assess whether their activities align with the sustainability criteria outlined in the Taxonomy Regulation and its delegated acts.

CSRD’s double materiality assessment requires firms to identify relevant topics for their sustainability reporting from dual perspectives: on how sustainability issues affect their performance, position, and development (the ‘outside-in’ perspective), and on the impact their activities have on people and the environment (the ‘inside-out’ perspective)1.

Companies will also need to report on intangibles — non-physical resources that contribute to value creation. This includes forms of capital like social, human, and intellectual capital, as well as value derived from research and development.

Both large companies and SMEs will be required to report using these indicators. However, the reporting standards for SMEs will be more flexible, and these standards are being developed alongside those for large firms.

How to communicate the sustainability information according to the Corporate Sustainability Reporting Directive?

Companies have to include sustainability information in their annual management reports. It should be available in an electronic XHTML format and have a digital ‘tag’. The goal of this measure is to make the reports machine-readable and easily fed into the European Single Access Point. The exact digitalisation standards are yet to be specified in the European Single Electronic Format (ESEF) Regulation and the European Single Access Point Regulation.

The reports will have to be prepared in accordance with the ESRS and submitted annually within the 12 months after the start of the financial year on January 1st. Large companies that are already subject to the NFRD will use the ESRS for the first time for the reports submitted on 1 January 2025. All other large firms will use the ESRS in 2026 for the first time. Standards for SMEs will apply in 2027.

Communicated information, including its compliance with the standards, will require assurance. The usual auditors and independent assurance services providers can verify the reports. Both of them should be accredited to evaluate whether the reports comply with requirements1. As soon as the Commission adopts sufficient sustainability audit standards, the scope will widen to a more detailed auditing process.

Why is it important to comply with the Corporate Sustainability Reporting Directive?

Not complying with the CSRD can result in administrative penalties and exclusion from investment portfolios. However, compliance with the regulation is not only important to avoid financial repercussions, but it also presents a growth opportunity — bringing about more clarity to the reporting process, attracting green investments, increasing a firm’s public accountability, and driving innovation.

Avoid sanctions and exclusion from investment portfolios

If a company is found to be non-compliant with the Corporate Sustainability Reporting Directive, the firm will face administrative sanctions. There are three possible penalties:

- A public statement about the breach.

- An order on the name of the entity requiring to change the conduct.

- Financial sanctions

It is up to member states to choose the penalty. They also have to define the extent of the sanctions when they transpose the directive to local law. Here are some examples:

According to the German version of the NFRD, firms are fined up to either € 10M, 5% of the annual turnover, or twice the amount of the profits gained or losses avoided because of the breach.9 French regulations impose penalties such as fines of up to €18,750 for failing to publish required sustainability reports, while more severe violations, such as obstructing external auditors or failing to ensure independent assurance, can lead to fines of up to €375,000 and prison terms of up to five years.

Another consequence of insufficient reporting is the loss of investments for the reasons of investor protection and upcoming legislation1. There is a growing awareness that sustainability-related issues can affect the firms’ performance which pushes away potential investors7. This risk will grow as sustainability information becomes ever more important throughout the financial system due to upcoming legislation targeted at enhancing green investments.

For example, the Sustainable Finance Disclosure Regulation (SFDR) compels investors to share how they account for the effects of their investments on people and the environment.10 The Taxonomy Regulation is another legislation that increases the demand for sustainability information and requires firms under the scope of the sustainability reporting directive to disclose the extent to which their activities are environmentally sustainable according to the taxonomy.

Harmonised reporting standards reduce cost and confusion

Harmonisation of the reporting standards will simplify reporting2, as enterprises would no longer have to deal with overlapping standards and inconsistent requests from stakeholders. The common framework will be a single, easy-to-use reporting system that reduces confusion and encourages collaboration. It will help companies get the information they need from partners like suppliers, clients, and investors without repeatedly asking for more details. According to the European Parliament, the decrease in such requests will save € 24 200 - 41 700 per company annually.4

Monetise sustainability efforts

By adopting non-financial reporting early, companies can take advantage of the growing focus on sustainability. This reporting can also enhance how the company is seen by key stakeholders1. Financial market participants such as investors and banks increasingly need information from businesses on their impacts on the environment and people to comply with disclosure requirements under the SFDR. Reliable reporting enhances investors’ engagement by enabling them to account for sustainability-related risks.

Additionally, the importance of making quantifiable and transparent sustainability claims is gaining popularity among consumers as they become more aware of greenwashing. A recent study indicated that two-thirds of consumers are willing to pay extra for sustainable products.11 Taking responsibility for their impacts helps firms harness public trust and acquire new consumers.1

Besides being important for various stakeholders, understanding the performance of the non-financial indicators can bring about new insights and innovation to the production processes. For example, decreasing costs by reducing energy consumption or monetising waste.

To circumvent the sanctions and utilise the benefits of the regulation, it is necessary to comply. However, it is often not clear where to start.

How to set up a reporting process in accordance with the Corporate Sustainability Reporting Directive?

The Corporate Sustainability Reporting Directive makes it mandatory to report on sustainability indicators as defined by the ESRS, but adjusting to the new requirements is not easy, and firms have to start preparing now.

Step 1: Supply chain collaboration

Begin with harnessing cooperation along your supply chains to get the information you need for reporting purposes from your business partners (suppliers, clients, and investee companies). This might be done through contractual agreements that ensure data sharing across your supply chain for the purpose of reporting in line with the ESRS.

Step 2: Collect and audit sustainability information

Set up your team and find auditing agencies to aid you in the collection and substantiation of the required sustainability information. Choose a reliable and scalable medium where the collected information can be stored in an XHTML format and from which it can be fed into the European Single Access Point with a digital ‘tag’. Currently, the majority of companies are accustomed to emailing PDF and Excel documents upon request, however, this way of data sharing is neither scalable nor secure.

Step 3: Keep an eye on the legislative procedure

Pay extra attention to the standard-setting by the European Financial Reporting Advisory Group, EU Taxonomy Delegated Acts, European Single Electronic Format Regulation, European Single Access Point Regulation, and the transposition of the directive in EU member states.

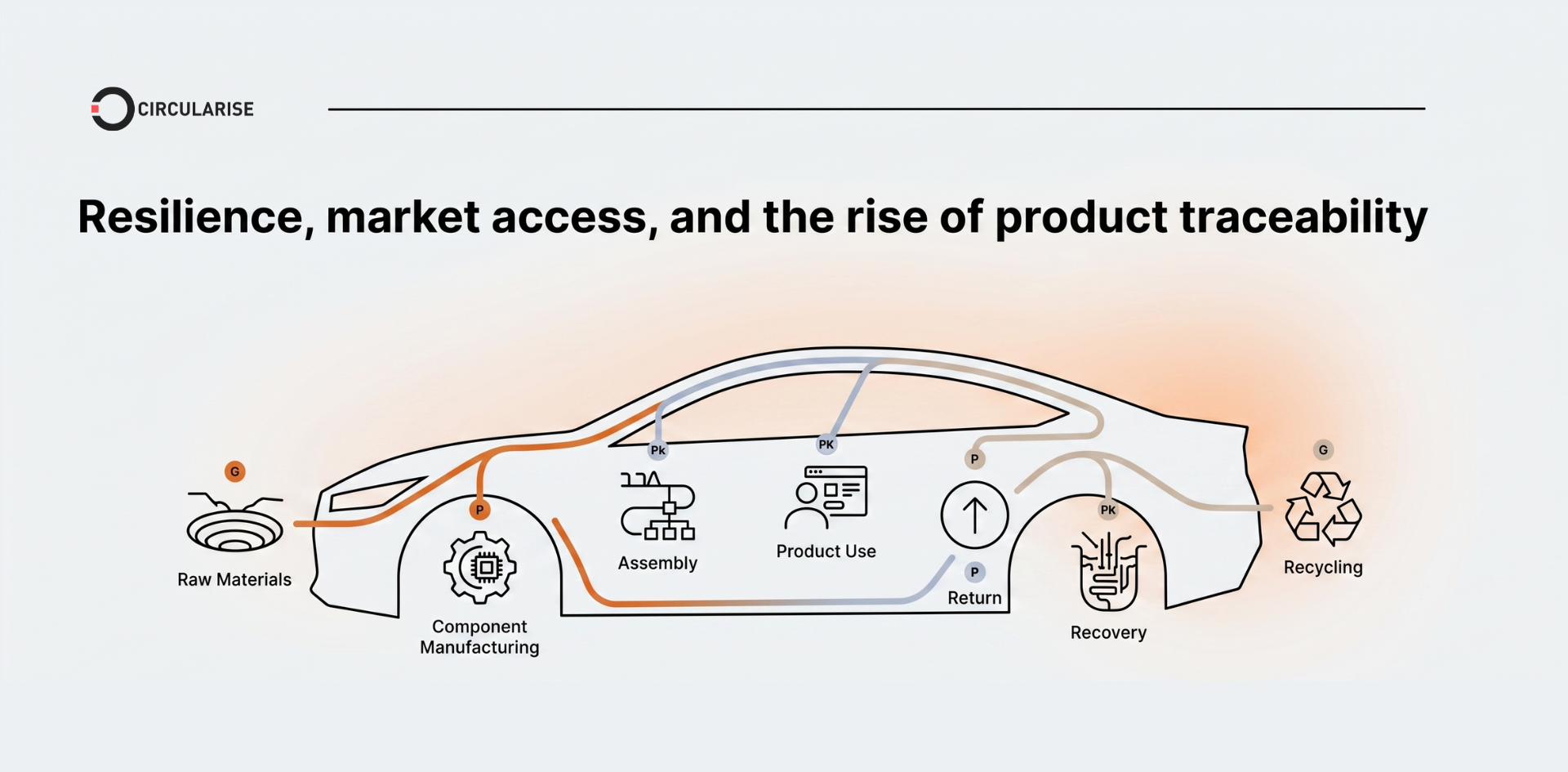

Step 4: Take steps to increase supply chain traceability

While full supply visibility is not currently required by the regulation, there are several key benefits. Awareness of ongoing activities enables you to evaluate business practices across a wide range of indicators, including social, environmental, and governance criteria, ensuring readiness to meet any standards. Additionally, this visibility helps substantiate sustainability claims, enhancing the credibility of reports for stakeholders such as governments, investors, and consumers. Moreover, it provides valuable insights for businesses to identify risks and inefficiencies across the supply chain, optimise performance to reduce costs and resource use, as well as leverage data-driven insights for more informed strategic decision-making.

How Circularise can help with complying with the Corporate Sustainability Reporting Directive?

To ensure you know what is happening across the supply chain, continually tracking the impact and chain of custody of all material that passes through a manufacturing company is required. However, this is a significant undertaking and presents a web of challenges from resourcing, to data integrity, and protecting company intellectual property. This is why Circuarise has developed a patented blockchain-powered traceability platform, which provides supply chain traceability that can not only be trusted but also integrated with existing operational processes. Read more about how we helped achieve visibility into the Porsche supply chain.

Conclusion

As regulatory frameworks like the Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CS3D or CSDDD) are reshaping the business landscape, supply chain traceability has become a necessity.

The demand for detailed and transparent sustainability reporting underscores the importance of collaboration, innovation, and robust data systems across the entire supply chain. However, achieving compliance requires a strategic approach to supply chain traceability. Companies must balance transparency with the protection of proprietary information, all while navigating complex reporting standards and processes.

Traceability platforms, like Circularise, offer a secure and scalable way to meet these challenges, empowering companies to share essential data responsibly. By adopting such solutions, businesses can turn regulatory compliance into a competitive advantage, driving progress toward a more sustainable and circular economy. The time to act is now — because the future of responsible business depends on it.

Circularise is the leading software platform that provides end-to-end traceability for complex industrial supply chains. We offer two traceability solutions: MassBalancer to automate mass balance bookkeeping and Digital Product Passports for end-to-end batch traceability.

.png)