Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

On 26 February 2025, the European Commission proposed the first Omnibus package, Omnibus I, aimed at helping EU companies meet their sustainability obligations by simplifying certain sustainability reporting legislation. The vote on 3 April 2025 approved the proposal’s “stop-the-clock” mechanism, making headlines across Europe as businesses and stakeholders look to understand the implications and how to implement the changes. "Stop-the-clock" refers to an immediate change in deadlines regarding certain directives within the scope of the omnibus.

Despite the simplifications, the core objectives of these regulations remain unchanged. They continue to apply to non-EU firms as well, ensuring that external companies also meet the EU’s sustainability standards.

In this article, we will break down the main changes which have been proposed, as well as those which have already been approved, such as the “stop-the-clock” mechanism. We will examine the changes – both proposed and those already adopted – and discuss how they impact businesses, as well as the next steps your company can take to stay ahead of the regulatory changes.

What is the EU Omnibus?

The Omnibus is a proposed regulation to simplify certain legislation within the EU in one package. The primary goal of this simplification is to enhance the competitiveness of EU companies, making it easier for them to comply with sustainability requirements and enabling them to better compete in global markets. This will help businesses make advancements in sustainability reporting by reducing administrative burdens.

Which legislations are affected by the Omnibus proposal?

The European Commission's Omnibus Simplification Package proposes updates and clarifications to key sustainability regulations, aiming to streamline requirements and ease administrative burdens. The following regulations are those impacted by the Omnibus changes:

The vote on the “stop-the-clock” mechanism has approved certain proposals, while others still remain to be voted on. Here is a list of the rules that have already been accepted, as well as those that are still awaiting a vote.:

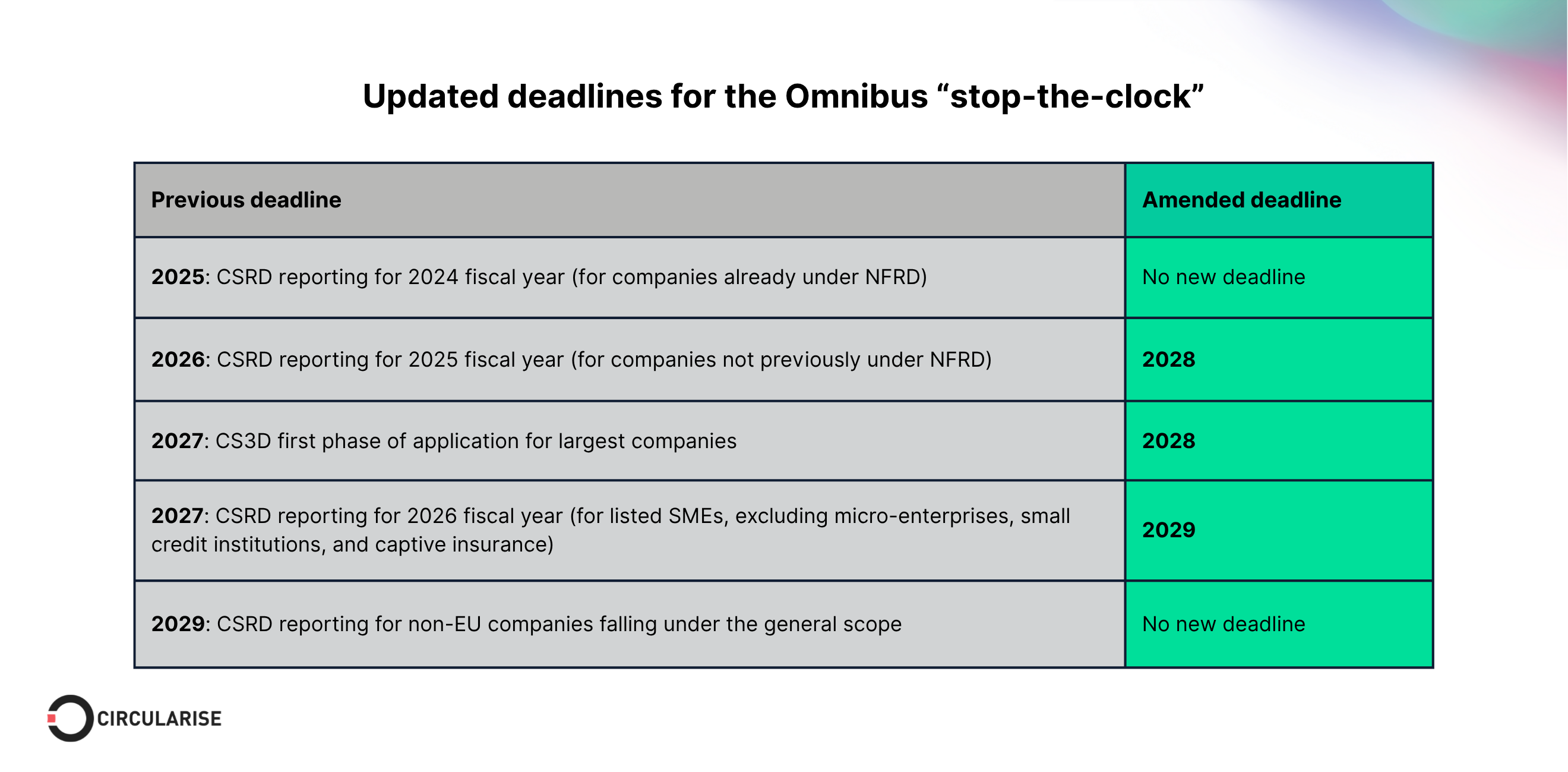

Omnibus rules approved: Key changes confirmed (as of July 2025)

Scope: Enterprises with over 500 employees already subject to the Non-Financial Reporting Directive (NFRD).

Deadline: No change. Companies must submit their CSRD-compliant reports for the financial year 2024 in 2025, as originally scheduled.

Wave 2: Two-Year Delay

Scope: Large non-listed companies and groups exceeding specific thresholds (e.g., 250+ employees or €40 million in net turnover).

Previous Deadline: 2026 (reporting on financial year 2025).

New Deadline: 2028. Companies now need to submit their reports on the financial year 2025 by 2028.

Wave 3: Two-Year Delay

Scope: Small and medium-sized public interest companies.

Previous Deadline: 2027 (reporting on financial year 2026).

New Deadline: 2029. Reporting for the financial year 2026 is now due in 2029.

Wave 4: No Change for Non-EU Companies

Scope: Non-EU companies operating in the EU market.

Deadline: No change. These companies must submit their CSRD reports for the financial year 2028 in 2029.

Figure 1: A table showing the changes in deadlines for CSRD and CS3D in light of the Omnibus “stop-the-clock” mechanism.

CBAM accepted changes

As part of the Omnibus I package, the Council and European Parliament have reached a provisional deal to simplify the EU's Carbon Border Adjustment Mechanism (CBAM), aiming to reduce compliance costs and administrative burden - especially for SMEs - without weakening climate goals. The reform retains coverage of around 99% of embedded emissions in CBAM goods.

Key changes include a new 50-tonne annual import threshold per importer, replacing the previous exemption for low-value goods. This broader de minimis exemption is expected to relieve many small importers from CBAM obligations. The agreement also introduces streamlined processes for importer authorisation, data collection, emissions calculation and verification, liability estimation, and recognition of carbon costs paid in third countries. Rules on penalties, indirect customs representatives, and financing the central CBAM platform were also clarified.

The agreement now awaits formal approval by both the Council and the European Parliament, with final adoption expected by September 2025. Once adopted, the changes will become legally binding.

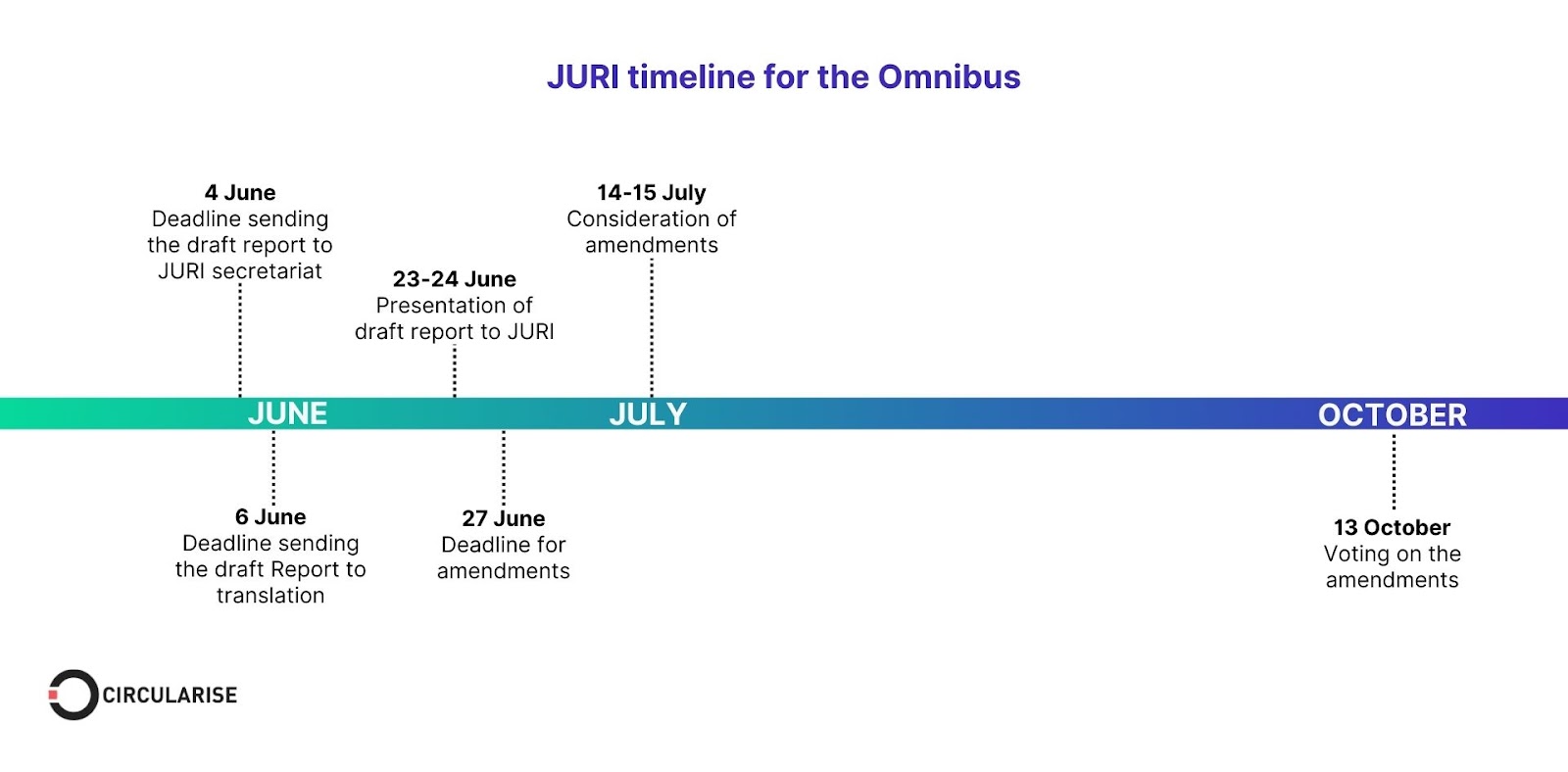

What happens next with the Omnibus?

The Omnibus stop-the-clock mechanism has been approved. However, the proposals regarding the changes to CSRD, CS3D, and Taxonomy have not yet been accepted. The European Parliament will not vote on these proposals until October 2025. Therefore, the original content of the legislation is applicable until then, meaning the scope and reporting requirements remain the same until the vote to change them has been approved.

Figure 2: Timeline of the European Parliament Committee on Legal Affairs (JURI) regarding what happens next with the Omnibus.

Pending vote: Omnibus rules still under discussion

As part of the ongoing negotiations surrounding the EU Omnibus package, a set of proposed changes has been introduced that could significantly impact large businesses operating within the European Union. While these proposals are still under discussion and have not yet been finalised or voted on, their potential scope and implementation may still evolve. Below is a summary of the key proposed revisions across various legislative instruments affected by the Omnibus.

Corporate Sustainability Reporting Directive (CSRD)The scope of the CSRD may be revised to apply only to companies with more than 1,000 employees, a shift that would exempt a broader swathe of smaller entities. Alongside this, the European Commission has proposed simplifications to the European Sustainability Reporting Standards (ESRS), including changes to sector-specific ESG disclosures. These measures aim to reduce administrative burden while maintaining the integrity of reporting. Additionally, the value chain reporting requirements would be reinforced through a strengthened “value-chain cap,” potentially placing more emphasis on traceability within supply chains.

Corporate Sustainability Due Diligence Directive (CSDDD)Proposals under the Omnibus package suggest narrowing the due diligence obligations to direct business partners only, thereby limiting the scope of liability unless a company has plausible knowledge of adverse impacts further down the value chain. The penalty framework would also be adjusted: rather than establishing EU-wide civil liability provisions, enforcement would be delegated to national frameworks, allowing for greater flexibility at the member state level.

EU Taxonomy RegulationTo ensure consistency with the revised CSRD thresholds, application of the EU Taxonomy could be limited to companies with more than 1,000 employees. A new opt-in mechanism is also being proposed, giving companies greater discretion over participation. Importantly, the number of mandatory reporting templates would be significantly reduced by approximately 70% in an effort to streamline compliance requirements and focus on material disclosures.

Want to learn more about this article?

Circularise is the leading software platform that provides end-to-end traceability for complex industrial supply chains. We offer two traceability solutions: MassBalancer to automate mass balance bookkeeping and Digital Product Passports for end-to-end batch traceability.

How will Omnibus affect you?

Stay ahead of regulatory changes. Confidently navigate the evolving compliance landscape and turn new sustainability requirements into strategic advantage with Circularise..

On 26 February 2025, the European Commission proposed the first Omnibus package, Omnibus I, aimed at helping EU companies meet their sustainability obligations by simplifying certain sustainability reporting legislation. The vote on 3 April 2025 approved the proposal’s “stop-the-clock” mechanism, making headlines across Europe as businesses and stakeholders look to understand the implications and how to implement the changes. "Stop-the-clock" refers to an immediate change in deadlines regarding certain directives within the scope of the omnibus.

Despite the simplifications, the core objectives of these regulations remain unchanged. They continue to apply to non-EU firms as well, ensuring that external companies also meet the EU’s sustainability standards.

In this article, we will break down the main changes which have been proposed, as well as those which have already been approved, such as the “stop-the-clock” mechanism. We will examine the changes – both proposed and those already adopted – and discuss how they impact businesses, as well as the next steps your company can take to stay ahead of the regulatory changes.

What is the EU Omnibus?

The Omnibus is a proposed regulation to simplify certain legislation within the EU in one package. The primary goal of this simplification is to enhance the competitiveness of EU companies, making it easier for them to comply with sustainability requirements and enabling them to better compete in global markets. This will help businesses make advancements in sustainability reporting by reducing administrative burdens.

Which legislations are affected by the Omnibus proposal?

The European Commission's Omnibus Simplification Package proposes updates and clarifications to key sustainability regulations, aiming to streamline requirements and ease administrative burdens. The following regulations are those impacted by the Omnibus changes:

The vote on the “stop-the-clock” mechanism has approved certain proposals, while others still remain to be voted on. Here is a list of the rules that have already been accepted, as well as those that are still awaiting a vote.:

Omnibus rules approved: Key changes confirmed (as of July 2025)

Scope: Enterprises with over 500 employees already subject to the Non-Financial Reporting Directive (NFRD).

Deadline: No change. Companies must submit their CSRD-compliant reports for the financial year 2024 in 2025, as originally scheduled.

Wave 2: Two-Year Delay

Scope: Large non-listed companies and groups exceeding specific thresholds (e.g., 250+ employees or €40 million in net turnover).

Previous Deadline: 2026 (reporting on financial year 2025).

New Deadline: 2028. Companies now need to submit their reports on the financial year 2025 by 2028.

Wave 3: Two-Year Delay

Scope: Small and medium-sized public interest companies.

Previous Deadline: 2027 (reporting on financial year 2026).

New Deadline: 2029. Reporting for the financial year 2026 is now due in 2029.

Wave 4: No Change for Non-EU Companies

Scope: Non-EU companies operating in the EU market.

Deadline: No change. These companies must submit their CSRD reports for the financial year 2028 in 2029.

Figure 1: A table showing the changes in deadlines for CSRD and CS3D in light of the Omnibus “stop-the-clock” mechanism.

CBAM accepted changes

As part of the Omnibus I package, the Council and European Parliament have reached a provisional deal to simplify the EU's Carbon Border Adjustment Mechanism (CBAM), aiming to reduce compliance costs and administrative burden - especially for SMEs - without weakening climate goals. The reform retains coverage of around 99% of embedded emissions in CBAM goods.

Key changes include a new 50-tonne annual import threshold per importer, replacing the previous exemption for low-value goods. This broader de minimis exemption is expected to relieve many small importers from CBAM obligations. The agreement also introduces streamlined processes for importer authorisation, data collection, emissions calculation and verification, liability estimation, and recognition of carbon costs paid in third countries. Rules on penalties, indirect customs representatives, and financing the central CBAM platform were also clarified.

The agreement now awaits formal approval by both the Council and the European Parliament, with final adoption expected by September 2025. Once adopted, the changes will become legally binding.

What happens next with the Omnibus?

The Omnibus stop-the-clock mechanism has been approved. However, the proposals regarding the changes to CSRD, CS3D, and Taxonomy have not yet been accepted. The European Parliament will not vote on these proposals until October 2025. Therefore, the original content of the legislation is applicable until then, meaning the scope and reporting requirements remain the same until the vote to change them has been approved.

Figure 2: Timeline of the European Parliament Committee on Legal Affairs (JURI) regarding what happens next with the Omnibus.

Pending vote: Omnibus rules still under discussion

As part of the ongoing negotiations surrounding the EU Omnibus package, a set of proposed changes has been introduced that could significantly impact large businesses operating within the European Union. While these proposals are still under discussion and have not yet been finalised or voted on, their potential scope and implementation may still evolve. Below is a summary of the key proposed revisions across various legislative instruments affected by the Omnibus.

Corporate Sustainability Reporting Directive (CSRD)The scope of the CSRD may be revised to apply only to companies with more than 1,000 employees, a shift that would exempt a broader swathe of smaller entities. Alongside this, the European Commission has proposed simplifications to the European Sustainability Reporting Standards (ESRS), including changes to sector-specific ESG disclosures. These measures aim to reduce administrative burden while maintaining the integrity of reporting. Additionally, the value chain reporting requirements would be reinforced through a strengthened “value-chain cap,” potentially placing more emphasis on traceability within supply chains.

Corporate Sustainability Due Diligence Directive (CSDDD)Proposals under the Omnibus package suggest narrowing the due diligence obligations to direct business partners only, thereby limiting the scope of liability unless a company has plausible knowledge of adverse impacts further down the value chain. The penalty framework would also be adjusted: rather than establishing EU-wide civil liability provisions, enforcement would be delegated to national frameworks, allowing for greater flexibility at the member state level.

EU Taxonomy RegulationTo ensure consistency with the revised CSRD thresholds, application of the EU Taxonomy could be limited to companies with more than 1,000 employees. A new opt-in mechanism is also being proposed, giving companies greater discretion over participation. Importantly, the number of mandatory reporting templates would be significantly reduced by approximately 70% in an effort to streamline compliance requirements and focus on material disclosures.

Newsletter

Essential insights on traceability, DPPs, and ESG — read by 3,500+ executives

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Why do supply chain traceability and transparency remain important?

While the Omnibus proposes some adjustments, the core requirements of sustainability reporting legislation remain unchanged. Regardless of whether the changes are adopted, key obligations will still apply, and companies must integrate them into their operations. Here are some important rules of CSRD, CSDDD, Taxonomy and CBAM that remain unchanged:

Firms which are part of a larger group count in the 1000+ employee ratio

Rules and reporting deadlines for non-EU firms remain in place

Reporting obligation for CBAM importers above the threshold

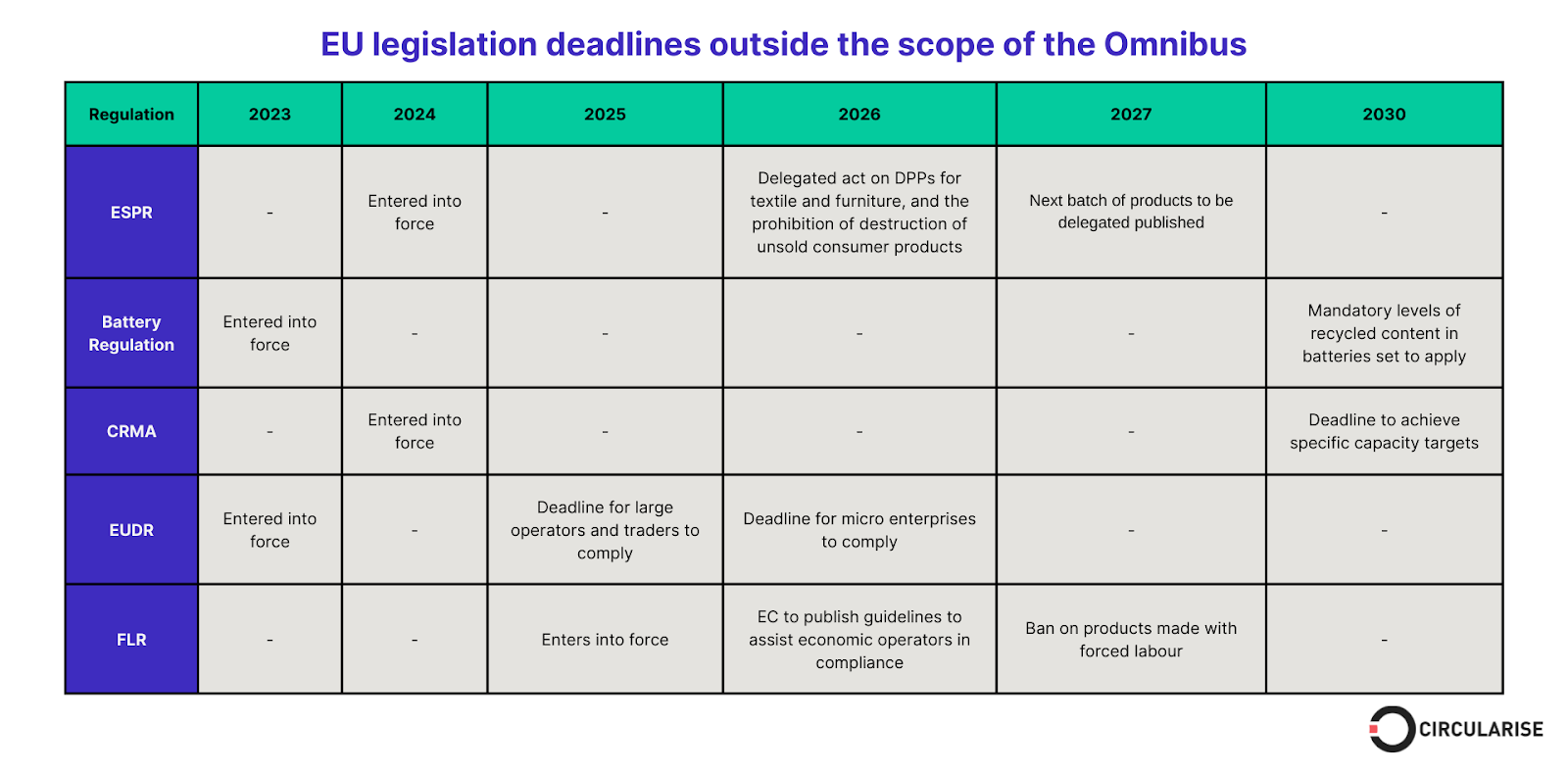

There are still many regulations within the EU Green Deal that call for traceability and transparency throughout the value chain, which the Omnibus does not affect. Additionally, businesses should take note that there are many other EU regulations that still require digital product passports (DPPs).

Figure 3: An overview of the various deadlines of EU regulations and directives that lie outside of the scope of the Omnibus and remain mandatory to follow.

Ecodesign for Sustainable Products Regulation (ESPR)

The ESPR aims to make products more sustainable by setting performance and information requirements across a product's lifecycle, including aspects like durability, reparability, and energy efficiency. It replaces the existing Ecodesign Directive, expanding its scope beyond energy-related products to include a broader range of goods.

One key element of the ESPR is the introduction of mandatory digital product passports (DPPs) for various categories of products. These passports will provide detailed, standardised information on a product’s environmental sustainability, enabling better consumer choices, more efficient recycling, and improved product tracking across the supply chain.

Companies will need to ensure their products comply with the new sustainability requirements, which may involve redesigning products, sourcing sustainable materials, and providing detailed product information to consumers.

Here are some of the key deadlines for the ESPR:

January 2026: Delegated Act on DPPs for textile and furniture products to be published

July 2026: Official prohibition of destruction of unsold consumer products

2027: Next batch of products to be regulated revealed

July 2027: Delegated Act on DPPs for textile and furniture products enters into force

Battery Regulation

The EU Battery Regulation focuses on the entire lifecycle of batteries, promoting sustainability, safety, and circularity. It sets requirements for the sourcing, production, labelling, and recycling of batteries to reduce environmental impact.

Companies involved in the battery supply chain must ensure responsible sourcing of materials, meet recycling efficiency targets, and provide detailed information on the carbon footprint and recycled content of their batteries in a battery passport.

Here are some of the key deadlines for the Battery Regulation:

The regulation entered into force in 2023, with various provisions becoming applicable between 2024 and 2030.

For instance, mandatory levels of recycled content in batteries are set to apply from 2030.

Critical Raw Material Act (CRMA)

The Critical Raw Materials Act (CRMA) aims to secure a sustainable and resilient supply of critical raw materials essential for the EU's green and digital transitions. It sets targets for domestic capacities in the extraction, processing, and recycling of these materials.

Here are some of the key deadlines for the CRMA:

25 March 2025: A list of strategic projects was announced.

2030: The EU aims to achieve specific capacity targets for critical raw materials.

EU Deforestation Regulation (EUDR)

The EU Deforestation Regulations (EUDR) aims to prevent the import and sale of products linked to deforestation. It requires companies to conduct due diligence to ensure that commodities like cattle, cocoa, coffee, palm oil, rubber, soy, and wood, as well as derived products, are not associated with deforestation.

In order to comply, businesses must establish robust traceability systems, collect geolocation data of production areas, and ensure compliance with local laws to demonstrate that their products are deforestation-free.

Here are some of the key deadlines for the EUDR:

30December 2025: Large operators and traders must comply

30 June 2026: Small and micro enterprises must comply.

Registration, Evaluation, Authorisation, and Restriction of Chemicals Regulation (REACH)

REACH is a comprehensive regulation governing the production and use of chemical substances in the EU. Having been in force in 2007 with reporting obligations since 2018, it requires companies to identify and manage risks associated with chemicals they manufacture and market in the EU.

Companies must ensure all substances they manufacture or import are registered with the European Chemicals Agency (ECHA). They must also communicate safety information down the supply chain and comply with any restrictions or authorisations applicable to their substances.

EU Regulation on Prohibiting Products Made with Forced Labour on the Union Market

The EU Regulation on Prohibiting Products Made with Forced Labour on the Union Market, also known as the Forced Labour Regulation (FLR), entered into force in December 2024. This regulation prohibits the sale of products made with forced labour within the EU market, regardless of their origin. It empowers authorities to investigate and remove such products from the market.

Companies must conduct thorough due diligence to ensure their supply chains are free from forced labour. This involves assessing suppliers, implementing robust compliance systems, and being prepared for potential investigations by authorities.

Here are some of the key deadlines for the FLR:

14th December 2027: The ban on products made with forced labour will be enforceable.

13th December, 2025: EU Member States are required to designate their competent authorities responsible for enforcing the regulation.

13th June, 2026: The European Commission is expected to publish guidelines to assist economic operators in complying with the FLR.

Emission Trading System Directive (ETS)

The EU ETS is a cornerstone of the EU's policy to combat climate change, operating on a cap-and-trade principle to reduce greenhouse gas emissions cost-effectively. Companies in energy-intensive sectors must monitor and report their emissions accurately, acquire sufficient allowances to cover their emissions, and explore opportunities to reduce emissions to lower compliance costs.

Here are some of the key deadlines for the ETS:

2021-2030: Phase 1 of the ETS — the system operates in trading phases.

30 April every year: Annual compliance cycles require companies to surrender allowances equal to their emissions for the previous year by 30 Aprileach year.

End-of-Life Vehicles (ELV) Directive

The End-of-Life Vehicles (ELV) Directive (Directive 2000/53/EC) aims to reduce the environmental impact of vehicles at the end of their life by promoting recycling, reuse, and recovery of materials, while limiting hazardous substances in vehicle components. Manufacturers are required to offer free take-back services for end-of-life vehicles, ensuring they are properly treated and recycled.

The directive sets targets for recycling and recovery, mandating that at least 85% of a vehicle’s weight be recycled, and 95% be recovered. Vehicles placed on the market after 2003 must also be free from hazardous substances such as lead, mercury, cadmium, and hexavalent chromium, with limited exemptions.

These ongoing obligations focus on designing vehicles for easier recyclability, and manufacturers must report the percentage of recycled materials used in new vehicles.

Classification, Labelling and Packaging Regulation (CLP)

The European Union's Classification, Labelling, and Packaging (CLP) Regulation (EC No 1272/2008) aligns the EU system with the United Nations' Globally Harmonised System (GHS) to ensure a high level of protection for human health and the environment. This regulation standardises the classification and labelling of chemicals, facilitating their safe use and free movement within the EU market.

Companies involved in manufacturing, importing, or distributing chemicals within the EU must comply with the CLP Regulation by classifying, labelling, and packaging substances and mixtures according to its criteria. This includes updating labels to reflect new hazard classifications, ensuring online platforms clearly display hazardous properties, and adhering to specific labelling requirements for various packaging formats.

Businesses should also monitor and implement changes introduced by adaptations to technical progress (ATP), such as the 21st ATP, which requires compliance by September 2025.

What are the next steps for businesses?

Despite updates proposed in the Omnibus Package, businesses must still meet existing sustainability obligations. The extended timeline is a chance to strengthen, not postpone, compliance strategies. Inaction risks non-compliance, with potential penalties including fines or loss of EU funding and investment opportunities.

Businesses must therefore remain focused on complying with other essential regulations like the Ecodesign for Sustainable Products Regulation (ESPR), ensuring that their products meet sustainability requirements. Staying compliant with these regulations is crucial to avoid financial penalties and reputational damage.

Sustainability is a powerful long-term strategy that can create significant value and resilience for businesses. Maintaining transparency in ESG reporting is vital, as it helps meet stakeholder expectations, builds trust, and sustains a competitive edge in the evolving marketplace. By keeping a close eye on legislative developments and proactively adapting to regulatory changes, businesses can stay ahead of the curve and ensure they’re always prepared for new requirements and deadlines.

How will Omnibus affect you?

Stay ahead of regulatory changes. Confidently navigate the evolving compliance landscape and turn new sustainability requirements into strategic advantage with Circularise..

.png)